|

|  |

|

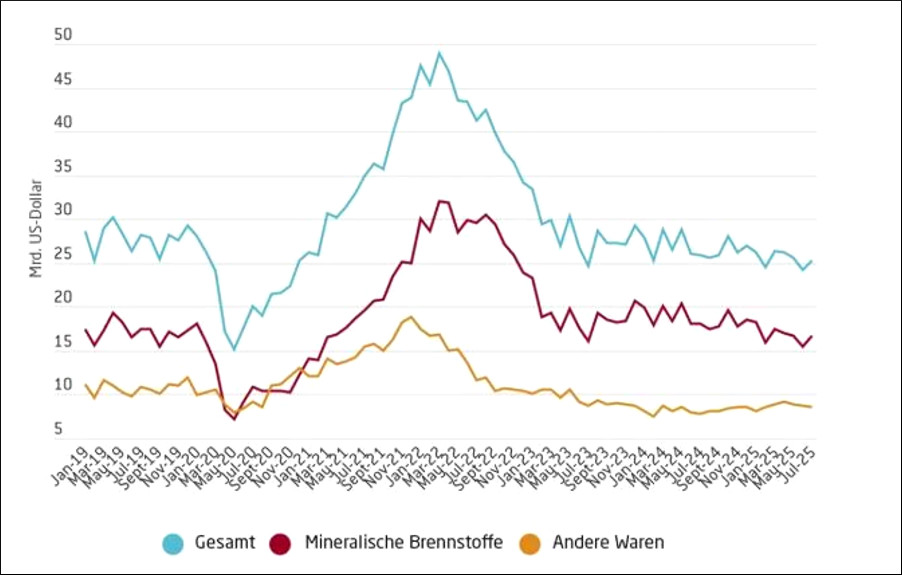

The limits of the Russian war economy  Figure 1: Russia's Exports Exports to 38 countries, which accounted for 80 percent (2019) of Russian imports and exports: the 27 EU countries, United Kingdom, USA, China, South Korea, Japan, India, Turkey, Switzerland, Norway, Brazil, Kazakhstan. Source: Russian foreign trade tracker Some Russian exports proved replaceable. Natural gas exports to the European Union, in particular, were largely replaced by liquefied natural gas from the US and supplies from other countries. This caused significant problems for the state-controlled energy company Gazprom. Despite these losses, however, Russia's overall export revenues remained at a generally acceptable level. Furthermore, Russia has benefited greatly in recent decades from the increasing diversification of the global economy and the rise of new, influential trading partners. In 2000, the G7 countries accounted for 65 percent of global GDP, while the BRICS countries accounted for only 8 percent. By 2021, the G7 share had fallen to 45 percent, while the BRICS share had risen to 26 percent. Adjusted for purchasing power parity, the BRICS share of global GDP, at 31.4 percent, even slightly exceeded that of the G7 countries, at 30.8 percent. The economic upheavals of the war led to the formation of new winners and losers – both within society and among the elites. It is not only the size of non-Western economies that is important, but also their increasing economic complexity. The Economic Complexity Index , which measures the complexity of a country's export basket, shows, for example, that China rose from 46th to 19th place between 2003 and 2021. Today, China is an industrial superpower that not only produces extremely cost-effectively, but is also capable of manufacturing a wide range of highly advanced goods and technologies. Had the invasion of Ukraine occurred in 2000, Western sanctions would have hit the Russian economy significantly harder. In the 2020s, however, non-Western countries were able to absorb a large portion of Russian exports and supply most of the necessary imports. For various reasons, including geopolitical and commercial considerations, many of them were also reluctant to join Western sanctions against Russia. This made Russia's economic decoupling from the global West a reality. This led to a particularly favorable development of relations between Russia and China, which has become one of Russia's most important trading partners in recent years. The role of the state Since the beginning of the war, the Russian state has also played an increasingly dominant role in the economy. Defense spending accounted for approximately 7.5 percent of GDP in 2025, equivalent to almost 40 percent of the Russian state budget . While this does not constitute a war economy in the historical sense—in the First and Second World Wars, the participating states invested nearly half of their GDP in their armed forces—Russia is nevertheless one of the economies with the highest military expenditures worldwide, both in absolute and relative terms. State-directed military mobilization contributed significantly to economic stabilization by mitigating unemployment and stimulating domestic demand. A substantial portion of economic growth in 2023 and 2024 can be directly attributed to military spending. Since taking office in 1999, Vladimir Putin has also systematically expanded state capacity in selected government institutions, particularly those responsible for economic policy (the Central Bank, the Ministry of Finance, and the Ministry of Economic Development). Simultaneously, flexible and resilient corporate structures have emerged in the Russian economy, and their professional management—in both the public and private sectors—has contributed to the economy's adaptability. Furthermore, Russia had already gained experience with at least a partial decoupling from the West and the associated economic crisis (2014–2021) since 2014. During this period, adaptation mechanisms developed, such as import substitution and new forms of cooperation between the state and the private sector, made it easier for Russia to respond to the drastic sanctions imposed from 2022 onwards. Winners and losers The economic upheavals of the war led to the formation of new winners and losers – both within society and among the elites. These shifts resulted from several interconnected processes: sanctions and the withdrawal of Western companies, the restructuring of international trade, the expansion of the Russian military-industrial complex, reconstruction in occupied territories, and payments to soldiers fighting in Ukraine. These processes are complexly interrelated and often have indirect consequences. For example, the massive hiring spree in the military-industrial complex created general upward pressure on wages, which in turn fueled a wage-price spiral and rising inflation. The central bank responded by raising the key interest rate. Combined with tax increases, these high interest rates led to a decline in investment in civilian sectors. While some industries and population groups benefited considerably, others were significantly disadvantaged. The expansion of the military-industrial complex also further changed the economic geography of Russia. Overall, the Russian war economy is characterized by very low unemployment – 2.2 percent in September 2025 compared to 4.3 percent in 2021 – and strong real wage growth. Real wages rose by 8.2 percent in 2023 and 9.1 percent in 2024, compared to 3.3 percent in 2021. However, this wage growth is highly unevenly distributed regionally and sectorally. Among the "winners"—in terms of rising bank deposits and incomes, as well as poverty reduction—are regions with particularly high army recruitment rates , including Tuva, Buryatia, and the Altai Republic. Tuva, which recorded the highest military losses at the end of 2023 with 140 soldiers killed per 100,000 inhabitants, also saw the strongest decline in poverty (five percentage points) and the strongest growth in bank deposits (plus 107.3 percent) in 2023 compared to 2021. Payments to the families of fallen soldiers were so substantial that they impacted regional income and poverty statistics. The expansion of the military-industrial complex further altered Russia's economic geography. In September 2024, authorities reported that approximately 600,000 people had been employed in the military industry since February 2022. This growth was concentrated in regions with existing military production facilities, such as Nizhny Novgorod and Sverdlovsk, which consequently experienced stronger wage increases than other regions. As the table below shows, the number of military factories per 100,000 inhabitants correlated with stronger wage growth in 2023 than in 2021. Sector-specific data also confirm that military-related industries recorded the highest wage increases. Figure 2: Relationship between wage growth and density of military factoriesSource: Author's own calculations based on data from Rosstat and data on military factories researched by BBC journalists In contrast, large cities like Moscow and St. Petersburg are among the losers in this development. While their advanced, post-industrial urban economies are large and flexible, they suffered most from deglobalization and the collapse of international economic relations. In terms of wage growth, Moscow ranked 77th out of 85 regions (Russian statistics also include occupied Crimea and Sevastopol), and St. Petersburg ranked 66th. Both cities showed weak performance in real incomes, bank deposit growth, and poverty reduction compared to 2021. There are also clear losers at the sectoral level, including oil and gas production and public services such as education, healthcare, and social services. The oil and gas sector was already characterized by high wages before the war, but faced considerable turbulence and restructuring after the invasion began. Weak wage growth in the public sector reflects chronic underinvestment, as government funds are increasingly diverted to the military rather than being invested in social spending. Overall, the militarization of the Russian economy and enforced import substitution led to a partial correction of the economic trends that had emerged since the collapse of the Soviet Union. The industrial working class and traditional industrial regions (including the military-industrial complex) were among the losers of economic change since the 1990s, resulting in widespread misery and poverty. Their situation has improved at least partially since 2022. Many Russians welcomed this development as a correction of deep-seated social and economic imbalances. However, this effect should not be overestimated, as the structural weaknesses of the war economy remain serious. Setback for the elite The war set in motion sweeping processes that led to a reorganization of the Russian economic elite. Some of this highly internationalized elite severed ties with Russia, while others strengthened their support for the existing political system and deliberately profited from the new situation. At least nine Russian billionaires on the Forbes list even chose to renounce their citizenship . Others withdrew their assets from Russia and moved abroad, but formally retained their Russian citizenship. Still others deliberately chose to stay and selectively acquired assets of Western companies that had withdrawn from the Russian market. According to The Bell, the revenues of these acquired companies amounted to around three trillion rubles (nearly 33 billion euros) in 2021, representing about 2.2 percent of Russia's GDP. Simultaneously, the state launched an unprecedented wave of nationalizations. According to the newspaper Novaya Gazeta, by March 2025, assets worth at least 2.56 trillion rubles (just over 27 billion euros) – almost two percent of GDP – had been nationalized. Before the war, Russian companies had a kind of "exit option" because they were embedded in the structures of domestic state capitalism and—in the case of the transnational capitalist class—in global networks. This dual integration allowed them to balance national and transnational capital interests against each other. However, the outbreak of war forced them to make a choice: stay or leave. The majority stayed, unwilling to relinquish their main sources of revenue. This increased their dependence on the Kremlin, whose enormous influence on the Russian economy has continued to grow since 2022. At the same time, the loss of this "exit option"—coupled with the fear of asset losses (for example, due to nationalizations)—could, in the long term, force the elite to develop strategies for asserting their political influence. Before the war, the Russian capitalist class was politically neutral precisely because it had an exit option. Instead of organizing politically, entrepreneurs could withdraw some or all of their capital from Russia. With the loss of this option, the remaining billionaires may now realize that they are permanently bound to the regime and that their assets are continuously at risk, necessitating new strategies for protection and adaptation. For the Kremlin, it will therefore become increasingly important to consider the interests of the economic elite and keep profitable business opportunities open in order to avoid growing discontent within the corporate sector. The war model is reaching its limits. While the Russian economy has proven resilient in the face of severe shocks, the limitations of the Russian wartime economic model are gradually becoming apparent. After two years of growth rates exceeding four percent, the central bank now forecasts growth of only 0.5 to 1 percent for 2025. Civilian industries are in a sustained decline . High interest rates are putting pressure on businesses, while investment, and especially capital investment, is decreasing. To finance the enormous military expenditures, the government continuously increased taxes. The corporate tax rate rose from 20 to 25 percent, the value-added tax was increased from 20 to 22 percent on January 1st of this year, and income tax now follows a progressive model with a top tax rate of 22 percent compared to 15 percent before the war. Furthermore, hundreds of thousands of skilled professionals emigrated, while Russia's deficit in education investment compared to leading economies, particularly China, widened. The resulting labor shortage is particularly burdensome in the civilian sector. New US sanctions against the major Russian oil producers Rosneft and Lukoil also left their mark, forcing Lukoil to divest assets in numerous countries. Technology transfer is now largely confined to non-Western states; however, China, in particular, due to its economic nationalism, is generally reluctant to share technologies—neither with Russia nor with other countries. Furthermore, real income growth in lower income brackets is partly statistically distorted. Prices for basic necessities such as food, housing, and services rise faster than those for other goods. The actual inflation rate for low-income households is therefore significantly higher than the official inflation figures. As a result, income gains for low-paid workers and pensioners are largely offset . Overall, it appears that after initial resilience and a surprising recovery, the Russian economy has once again entered a long-term period of stagnation, although its nature differs from the pre-war era. International economic relations are largely limited to non-Western countries, while the war effort is diverting resources from the civilian sector without generating any significant multiplier effects. Declining human capital and limited opportunities for technology transfer further worsen the long-term outlook. While “Fortress Russia” may be resilient, the development gap with the global North and successful emerging economies – particularly China – continues to widen. Under the current political and economic conditions, it seems highly unlikely that Russia can close this gap. Translation by Cornelia Gritzner & Claire Schmartz for Kontrast Translation Collective. https://www.rosalux.de/news/id/54251/die-grenzen-der-russischen-kriegswirtschaft Back Political scientist Ilya Matveev writes primarily about Russian and international political economy. |

|

||||||

|

|||||||